How to Purchase Reverse Mortgage and Use It to Fund Your Future

How to Purchase Reverse Mortgage and Use It to Fund Your Future

Blog Article

Unlock Financial Freedom: Your Guide to Buying a Reverse Home Mortgage

Understanding the intricacies of reverse mortgages is essential for homeowners aged 62 and older looking for economic liberty. As you consider this choice, it is vital to comprehend not only how it functions yet additionally the ramifications it may have on your financial future.

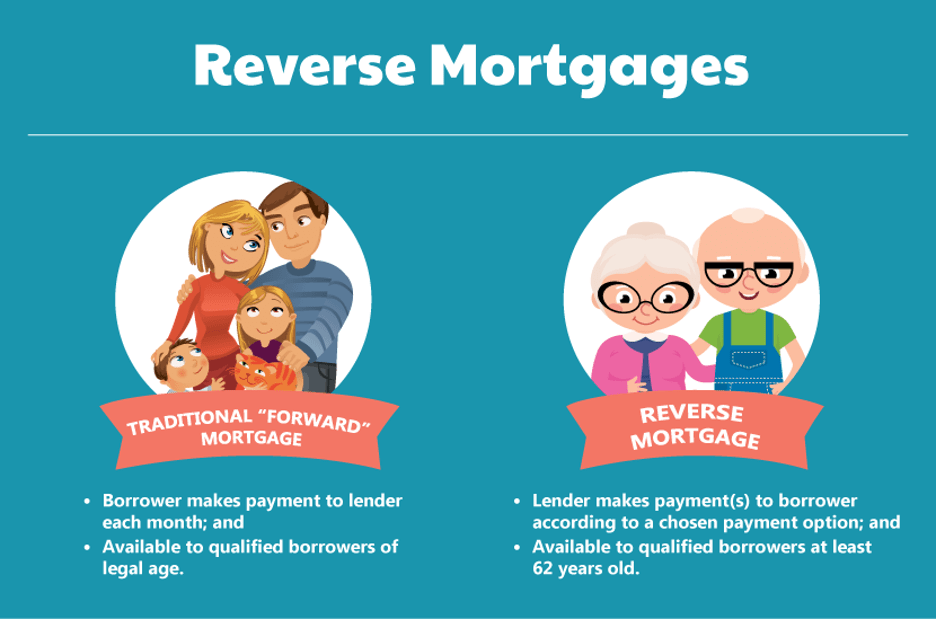

What Is a Reverse Mortgage?

The basic appeal of a reverse home mortgage lies in its prospective to boost financial versatility throughout retirement. Property owners can make use of the funds for various functions, consisting of medical costs, home renovations, or daily living costs, thus supplying a safety and security net during an essential stage of life.

It is important to recognize that while a reverse home mortgage permits raised capital, it likewise reduces the equity in the home with time. As passion accumulates on the exceptional finance balance, it is essential for possible customers to thoroughly consider their long-term financial strategies. Consulting with an economic advisor or a reverse mortgage professional can give beneficial understandings right into whether this alternative straightens with a person's economic objectives and conditions.

Qualification Needs

Recognizing the qualification demands for a reverse home loan is important for house owners considering this monetary option. To qualify, applicants have to go to the very least 62 years old, as this age criterion allows elders to accessibility home equity without regular monthly home loan payments. Additionally, the homeowner must inhabit the home as their main dwelling, which can consist of single-family homes, specific condominiums, and manufactured homes fulfilling certain guidelines.

Equity in the home is an additional crucial demand; property owners generally require to have a considerable amount of equity, which can be established with an appraisal. The quantity of equity offered will directly affect the reverse mortgage quantity. Moreover, applicants need to demonstrate the capacity to preserve the home, consisting of covering real estate tax, homeowners insurance policy, and maintenance prices, guaranteeing the property stays in good problem.

Additionally, potential consumers should go through an economic assessment to assess their revenue, credit report, and total financial circumstance. This analysis aids lenders identify the candidate's capacity to fulfill ongoing obligations connected to the building. Meeting these requirements is important for protecting a reverse home mortgage and making certain a smooth financial transition.

Benefits of Reverse Mortgages

Various benefits make reverse home loans an attractive choice for senior citizens seeking to boost their economic adaptability. purchase reverse mortgage. Among the key benefits is the capability to transform home equity right into money without the requirement for regular monthly home loan repayments. This feature allows seniors to access funds for various needs, such as clinical expenditures, home renovations, or daily living expenses, consequently easing monetary tension

Additionally, reverse mortgages give a security internet; seniors can remain to reside in their homes for as long as they meet the lending needs, cultivating stability during retired life. The earnings from a reverse mortgage can also be utilized Discover More Here to delay Social Safety and security benefits, potentially causing greater payouts later on.

In addition, reverse mortgages are non-recourse financings, implying that debtors will certainly never owe greater than the home's worth at the time of sale, shielding them and their successors from monetary liability. The funds received from a reverse home loan are typically tax-free, including another layer of economic relief. Overall, these advantages setting reverse mortgages as a practical remedy for senior citizens looking for to boost their economic circumstance while keeping their treasured home setting.

Fees and costs Included

When considering a reverse home loan, it's important to understand the numerous costs and charges that can influence the total economic image. Comprehending these expenses is crucial for making a notified decision regarding whether this monetary product is appropriate for you.

One of the main prices connected with a reverse home mortgage is the source cost, which can differ by lending institution but usually varies from 0.5% to 2% of the home's appraised worth. Furthermore, property owners should anticipate closing prices, which might consist of title insurance you can try here coverage, assessment fees, and credit record charges, typically totaling up to several thousand bucks.

An additional significant cost is home mortgage insurance policy premiums (MIP), which safeguard the loan provider against losses. This charge is normally 2% of the home's worth at closing, with a continuous annual costs of 0.5% of the remaining finance equilibrium.

Lastly, it is necessary to think about continuous prices, such as real estate tax, property owner's insurance, and upkeep, as the debtor stays in charge of these expenditures. By thoroughly reviewing these expenses and fees, homeowners can better assess the monetary effects of going after a reverse home loan.

Actions to Get Going

Obtaining begun with a reverse mortgage entails several key actions that can aid simplify the process and ensure you make informed decisions. First, assess your monetary situation and establish if a reverse mortgage aligns with your long-lasting objectives. This includes reviewing your home equity, present financial debts, and the necessity for extra earnings.

Following, research different lenders and their offerings. Look for trustworthy organizations with positive testimonials, transparent fee frameworks, and competitive rates of interest. It's vital to compare conditions and terms to discover the very best fit for your requirements.

After picking a lender, you'll need to complete a thorough application procedure, which typically requires paperwork of earnings, assets, and home information. Involve in a therapy session with a HUD-approved counselor, that will certainly offer insights into the ramifications and obligations of a reverse home mortgage.

Conclusion

In final thought, reverse mortgages provide a viable choice for seniors seeking to boost their financial security during retirement. By converting home equity into obtainable funds, house owners aged 62 and older can address different monetary needs without the stress of month-to-month payments.

Comprehending the complexities of reverse home loans is essential for homeowners aged 62 and older looking for economic liberty.A reverse home mortgage is an economic item created mostly for homeowners aged 62 and older, allowing them to transform a part of their home equity right into cash money - purchase reverse mortgage. Consulting with a reverse mortgage why not check here or a financial expert expert can give useful understandings into whether this option straightens with an individual's monetary objectives and scenarios

Furthermore, reverse home loans are non-recourse fundings, suggesting that consumers will certainly never owe even more than the home's value at the time of sale, protecting them and their successors from financial responsibility. In general, these benefits position reverse home mortgages as a sensible option for elders looking for to improve their economic situation while keeping their valued home setting.

Report this page